*This article was updated in May 2026 to reflect the latest Federal Budget announcements and proposed changes relating to Capital Gains Tax in Australia.

If you own an investment property or you are thinking about selling one, you’ve probably heard the term Capital Gains Tax. It is one of those phrases that can sound complicated, but at its core, it’s relatively straightforward.

At Keevers Group, we find many investors want a little clarification Capital Gains Tax works, when it applies and how much it might impact their final sale result. This guide breaks it down in simple terms so you can make informed decisions with confidence.

What Is Capital Gains Tax?

Capital Gains Tax (commonly referred to as CGT) is the tax you pay on the profit made when you sell an asset. In this case, your investment property.

It is important to understand that CGT is not a separate tax. It forms part of your income tax. The capital gain is added to your taxable income in the financial year you sell the property.

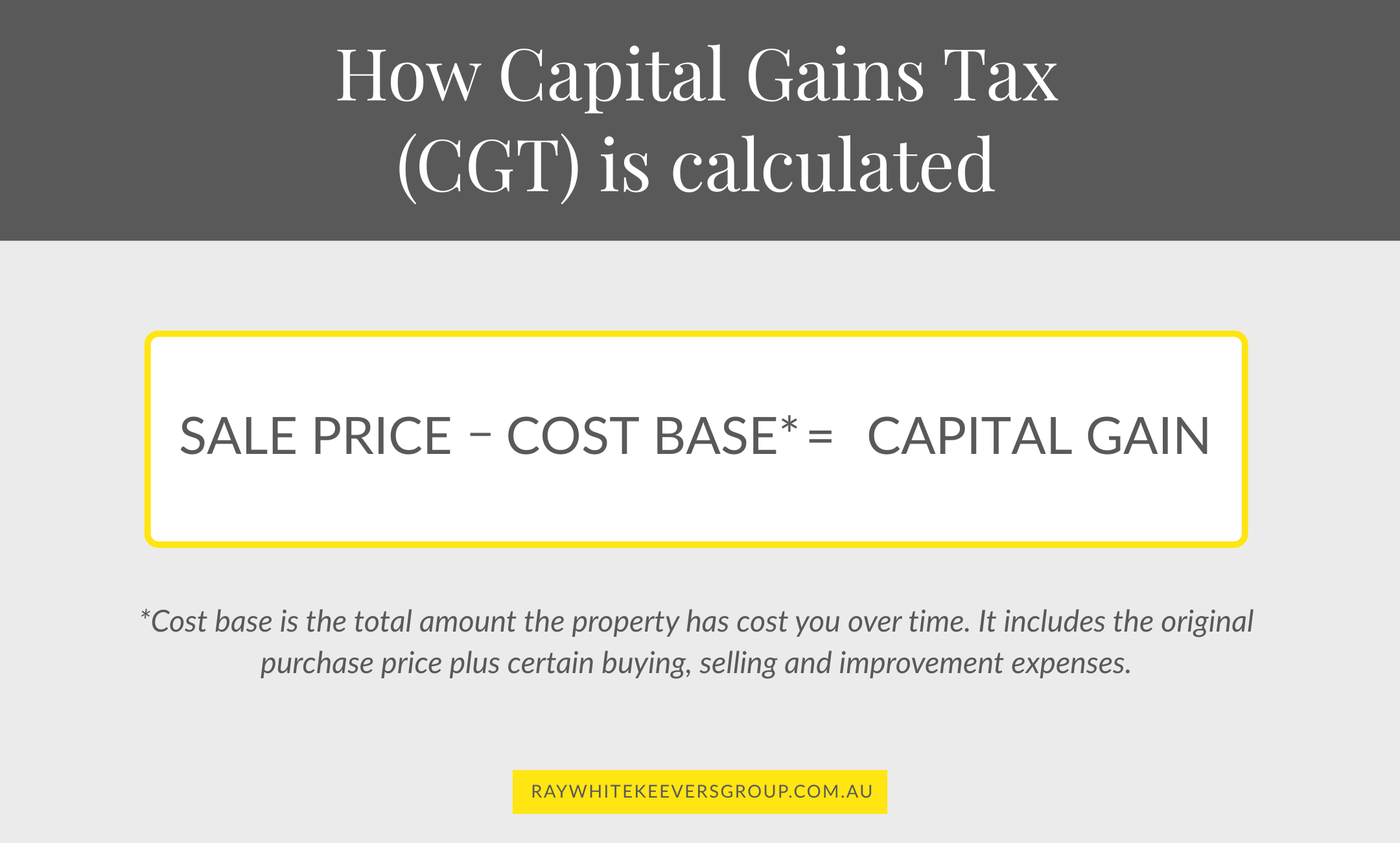

In simple terms: Sale price – minus your cost base* = capital gain. You are then taxed on that gain at your relevant income tax rate.

*Cost base is the total amount the property has cost you over time. It includes the original purchase price plus certain buying, selling and improvement expenses.

What Is Included in the Cost Base When Calculating Capital Gains Tax (CGT)?

Your cost base is not just the purchase price. It includes many of the costs associated with buying, holding and selling the property.

Your cost base can include:

The purchase price

Stamp duty

Conveyancing and legal fees

Buyer’s agent fees

Building and pest inspections

Selling agent commission

Advertising costs when selling

Capital improvements such as renovations, extensions or structural upgrades

Cost base does not usually include day to day repairs or maintenance, as those are typically claimed as deductions during ownership.

The 50% Capital Gains Tax Discount (And Proposed Changes)

One of the most important things investors should know is the current 50% CGT discount rule.

Under the current system, if you have owned your investment property for more than 12 months, you may be eligible for a 50% discount on the capital gain. This means only half of the gain is added to your taxable income.

This rule currently applies to individuals and most trusts. Companies are not eligible for the 50% discount.

However, Capital Gains Tax rules have recently become a major topic following announcements in the 2026 Federal Budget. The Federal Government has proposed significant changes to how CGT is calculated from 1 July 2027 onwards.

Under the proposed reforms:

The current 50% CGT discount would be replaced with an inflation-based system called cost base indexation

A minimum 30% tax on capital gains would apply in many cases

Transitional rules would apply for existing property owners

Investors purchasing newly built homes may still have access to the current 50% discount system as part of efforts to encourage new housing supply

Importantly, these changes are proposed to apply only to gains accrued after 1 July 2027, meaning existing ownership periods prior to that date would still fall under current rules.

At this stage, investors should view these reforms as an evolving area of tax policy rather than panic over immediate changes. Property remains a long-term investment strategy, and professional advice will become even more important as legislation develops.

A Simple Example

Let’s look at a straightforward example.

You purchased an investment property for $600,000. Your stamp duty and legal costs totalled $25,000. Over time, you completed $40,000 in capital improvements.

Your cost base is: $600,000 + $25,000 + $40,000 = $665,000

You later sold the investment property for $900,000.

Your capital gain is: $900,000 – $665,000 = $235,000

Property Investors should view CGT reforms as an evolving area of tax policy rather than panic over immediate changes.

Under The Current CGT Rules

If you owned the property for more than 12 months, you may currently qualify for the 50% CGT discount.

This means only half of the capital gain would be added to your taxable income: $235,000 ÷ 2 = $117,500 taxable capital gain

That $117,500 would then be taxed at your marginal income tax rate for that financial year.

Under The Proposed Federal Budget Changes

Under the proposed Federal Government reforms announced in the recent Federal Budget, the current 50% CGT discount may eventually be replaced with a different calculation method based on inflation indexation.

While the exact outcome will depend on future legislation and your individual circumstances, this could mean some investors pay more CGT on future property sales than they would under the current system.

Importantly, the proposed changes are expected to apply only to gains accrued after 1 July 2027, with transitional arrangements likely for existing property owners.

As these reforms are still proposals at this stage, it is important to seek professional accounting or financial advice before making decisions based on potential future tax changes.

Why Capital Gains Tax Should Not Cause Panic When Selling

It is common for investors to delay selling because they are worried about the tax bill. While CGT is an important consideration, it should always be viewed in context.

If your property has increased significantly in value, paying tax on a profit still means you have made a profit.

For many Perth investors, particularly along the coastline and in tightly held suburbs, recent growth has prompted a reassessment of their portfolios. Sometimes selling and reinvesting elsewhere can create stronger long term outcomes, even after tax.

While CGT is an important consideration when selling your home, it should always be viewed in context.

The Importance of Professional Advice

Capital Gains Tax can become more complex if:

The property was once your main residence

You have moved in and out of the property

You inherited the property

The property is owned in a trust or company

Before making any decisions, it is essential to speak with your accountant or financial adviser. They can calculate your exact position and help you understand the impact in your personal circumstances.

Why Staying Informed Matters

The recent Federal Budget proposals are a reminder that tax laws can evolve over time. Investors who purchased properties years ago under one set of expectations may soon be navigating very different rules around Capital Gains Tax and negative gearing.

While the proposed changes are still developing, they highlight the importance of reviewing your investment strategy regularly and seeking tailored financial advice before making major property decisions.

Thinking About Selling Your Investment Property?

Understanding Capital Gains Tax is part of smart investing. It should never be the sole reason to hold or sell, but it absolutely deserves careful planning.

If you are considering selling your investment property and would like to understand its current market value, our team can provide a confidential appraisal and talk through the local market conditions.

Q2 2026 Market Update: Perth’s property market continues to outperform many other Australian capitals, despite national uncertainty and proposed property tax reforms. Discover the key trends shaping the market, what they mean for buyers, sellers and investors, and why local knowledge matters more than ever.

Winter weather can quickly expose maintenance issues around your home or investment property. Discover eight simple preventative maintenance tips to help protect your property, avoid costly repairs and keep your home in top condition throughout the cooler months.